Life insurance provides valuable death benefit protection, however it can also offer added flexibility when used as a supplemental cash flow tool.

Life Insurance in Retirement Planning

A Properly Designed Life Insurance Policy Can Provide:

Income tax-free death benefit protection

Tax advantaged cash value growth potential

Supplemental retirement cash flow, through tax advantaged withdrawals and/or loans

Where does Cash Value Life Insurance fit?

Clients who need a retirement vehicle with downside protection

High income individuals looking to minimize taxation on earnings

For those who have maximized funding on qualified/non-qualified plans

An Insurance Solution

Death benefit protection during the accumulation years

Accessible cash value during retirement years

Life insurance becomes an income producing asset in the retirement portfolio

How it Works

Apply for a permanent life insurance policy using Indexed Universal Life (IUL) or Variable Universal Life (VUL)

Based on cash value performance, the policy will grow on a tax-deferred basis

Distributions can be withdrawn/loaned for any purpose

Additional Benefits Created

Provide additional income to pay for your child’s college expenses

Help supplement a gap in retirement before social security begins

Create a steady cash flow after life expectancy once all other assets have been depleted

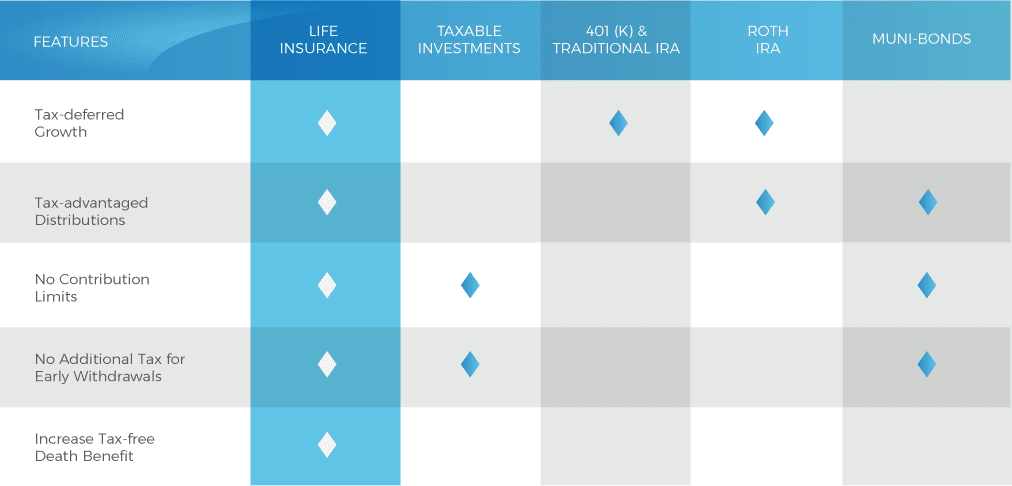

Listed below are the advantages of using cash value life insurance in everyday retirement planning

Our Strategies

Contact Us

Simplicity BKA Financial

Privacy Policy

Social Media

FOR FINANCIAL PROFESSIONAL USE ONLY. NOT FOR PUBLIC DISTRIBUTION.

BKA Financial, a Simplicity Company, is an insurance producer and does not provide legal, tax, or investment advice. SEC/State registration does not imply a specific level of skill or endorsement by regulators. All investing involves risk and loss of principal; no strategy guarantees profit. Insurance guarantees are subject to the claims-paying ability of the issuing carrier.

© Simplicity Group - All Rights Reserved. SWG#5483906-0526